In the movie Ghostbusters, Egon Spengler tries to describe the amount of psychokinetic energy currently in the New York area using an analogy – a Twinkie:

Egon Spengler: I’m worried, Ray. All my readings point to something big on the horizon.

Winston Zeddemore: What do you mean, big?

Egon Spengler: Well, let’s say this Twinkie represents the normal amount of psychokinetic energy in the New York area. Based on this morning’s reading, it would be a Twinkie thirty-five feet long, weighing approximately six hundred pounds.

Winston Zeddemore: That’s a big Twinkie.

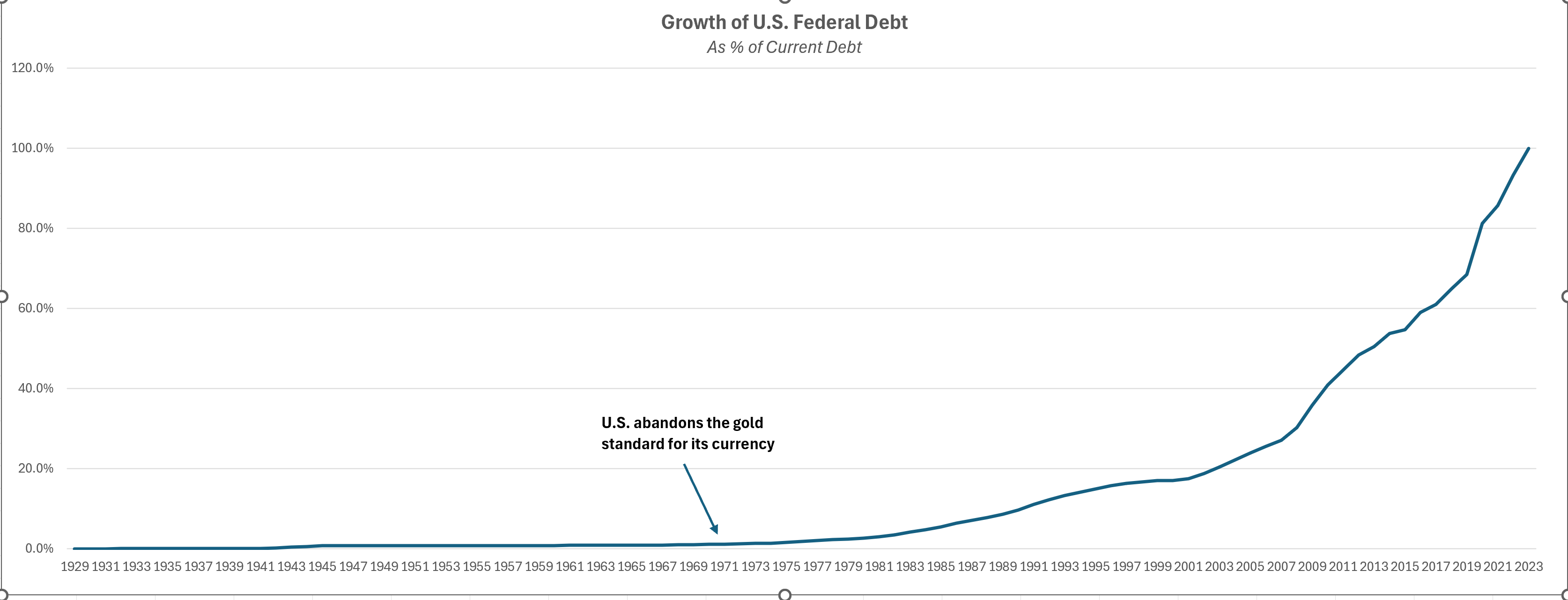

I have been trying to get my head around the size of the national debt of the United States, which, at the time of this post, stands at $34.8 trillion. First, I developed an abbreviated number line in order to see what the number one trillion looked like.

So, one trillion is a one followed by 12 zeros. Thus, $34.8 trillion is $34,800,000,000,000. That’s a big Twinkie.

To further my perspective, if the debt magically stopped growing and the U.S. government committed to paying down the debt by a very modest $1 every second of every minute of every hour of every day ($86,500 per day), how long would it take to repay $34.8 trillion?